In an economy driven by AI and digital technology, small, focused, and nimble companies can leverage technology platforms to effectively compete against big, mass-market entities. The small can do this because they can rent scale that companies used to need to build. The small can rent computing in the cloud, rent access to consumers on social media, rent production from contract manufacturers all over the world—and they can use artificial intelligence to automate many tasks that used to require expensive investments in equipment and people.

Because AI is software that learns, it can learn about individual customers, allowing companies built on rentable tech platforms to easily and profitably make products that address very narrow, passionate markets—even markets of one. The old mass markets are giving way to micro markets.

-Hemant Taneja in his book Unscaled

When I first started reading up on Upstart, Taneja’s words came to my mind. This is exactly what Upstart, the company I’m going to deep dive on today, is doing.

Here’s the outline for today’s deep dive:

1) Upstart and their reason to exist

2) Management

3) Business model (how do they make money?)

4) Competitive Advantages

5) The Numbers

6) What I like about the company

7) Risks

8) Competitors and the Valuation

9) Final thoughts

1) Upstart and their reason to exist

Upstart is an AI-driven lending platform that uses 1,600+ variable inputs to determine the creditworthiness of a borrower, which in turn leads to a superior loan product with improved economics between both the lender and consumer. Its platform aggregates demand for consumer loans and connect the borrowers to capital from their bank partners and also institutional investors.

By leveraging the use of AI and machine learning, consumers who use Upstart benefit from higher approval rates, lower interest rates, and a highly automated and efficient experience. Long gone are the days where you would have to queue to get yourself a loan from the bank. On the other hand, bank partners benefit from access to new customers, lower fraud and loss rates, and increased automation throughout the lending process. This increased automation saves both the consumers’ and bank partners’ time and resources. I will share more on this later.

Since Upstart is all about lending, let’s begin by thinking about what actually happens when you lend someone money. When you lend someone money, they either pay it back or they don’t. It’s a binary outcome.

Given that it’s a binary outcome, it makes me surprised when I learned that Upstart’s main source of lending is from unsecured personal loans. This means that the bank partners/institutional investors are backed by nothing. If the borrower decides to not pay back, there’s technically nothing that they can do given that the loan is not collateralized.

For a company like Upstart who was founded in 2012, it tells us 2 things:

The efficacy of their platform. If their AI platform wasn’t good at identifying the “true risk” of the borrower, they would probably already be out of business by now.

The company’s decision to start off from unsecured personal loans was a deliberate one. Personal loans are the most flexible type of loan, as they can be used for any purpose. It sounds crazy for a lending company to start from the riskiest category of loans.

According to Head of Product Paul Gu,

“We always felt that if we started from the riskiest category, it would be easier to go from personal loans to other types of loan products, than the other way around, where you start from something very safe and limited, it would be really difficult to get out of that box, and go to other spaces.”

What’s Upstart’s main reason for existence?

Upstart’s mission is to enable effortless credit based on true risk.

Unlike Upstart, most banks currently use the FICO score and a limited number of variables to determine a borrower’s creditworthiness. As a result, this leads to the problem where millions of people are being declined simply because of poorer credit scores and millions of people paying more interest just to subsidize losses elsewhere.

“Every loan that doesn’t default was priced too high, and every loan that defaulted shouldn’t have been approved in the first place.” - Paul Gu

This is the problem that Upstart wants to solve, and their most recent performance definitely shows that they’re firing on all cylinders.

Let’s take a look at the founders at the helm.

2) Management

If you’ve heard about Upstart somewhere, you would probably know of their ex-Googlers management team. What makes this even more amazing is the fact that these trio founders have stuck together with each other for the past 9 years. How many companies that started with 3 founders are still running the company together after so many years? Few, I think.

Founder-led companies outperform the rest. In an in-depth study conducted by Bain & Co, it was found that an index of S&P 500 companies in which the founder remained deeply involved “performed 3.1 times better” over the 15 years ranging from 1999 to 2014. According to the study, the reason for the outperformance is due to the “founder’s mentality”. Founders often waged war on industry norms to the benefit of underserved customers (Netflix, Tesla) and they often see the companies they built as a life-long project and are more inclined to make decisions that maximize the long-term success.

From my past two articles on Peloton and Crowdstrike, you can probably tell that I love reading a lot on the management team. The reason is simple. In the past, knowing how to select companies based on quantitative characteristics will make you stand out as an investor. Fast forward to today, the numbers are usually available to everyone, but what cannot be seen from the numbers are the qualitative characteristics inside the company. When we invest in a company, we’re investing in the people managing the assets, not the other way round.

Let me first give a short introduction to the team of founders. Dave Girouard is the execution guy, Paul Gu’s the data science and technology guru and we have Anna Counselman who is in charge of people and operations. According to Dave Girouard, this current role assignment is very reflective of each of their strengths as a team. A little more about their background:

1) Dave Girouard

Before he even started Upstart, Dave Girouard had forged an impressive resume. After leaving the world of consulting behind, he became a product manager at Apple (pre-Steve Jobs' return), gained formative startup experience at Virage (which took a stab at image recognition software in the dot-com era), all before arriving at Google in 2004.

Over an eight-year stint as the Enterprise President at Google, Girouard scaled the enterprise apps division to its first billion dollars, which included everything from figuring out the "yellow box" of Google Search Appliance to turning Gmail, Google Docs, and Google Calendar into a suite of products.

However, he knew what he wanted was to really build a billion-dollar revenue company of his own. Hence, without a clear idea of what Upstart was going to be, he quietly started trying to find co-founders while at Google. The process of finding a co-founder was arduous, to say the least. There were many of his friends and colleagues who found his initial idea interesting, but not interesting for them to want to take a leap to join him.

Dave Girouard then resigned without any co-founders to pursue his idea fully. It was right when he left that he got introduced to Paul Gu, the data science guru. They chatted on the phone, that’s when he realized that Gu was building something similar to what he was thinking about. Gu then emailed his entire model to him, and not soon after Gu flew over to meet him to see if they could work something out, and we knew what eventually happened.

2) Paul Gu

Gu is the Head of Product and Data Science at Upstart. If you’ve watched older videos of Gu talking at conferences, you’ll soon realize that he’s a young, budding tech visionary. The ability to explain complex concepts and simplify them shows us how much Gu understands what he’s doing.

Gu is part of Peter Thiel’s (Paypal & Palantir founder, early investor in Facebook) 20 under 20 fellowship, a program that is reserved for the brightest minds in the country. It's a two-year program that grants $100,000 to young people who want to skip or step out of college. By being part of Thiel’s program, you get access to his network of investors and also high-level expertise from all fields that you can’t find anywhere else. Notable recipients of this award include the founder of Ethereum blockchain, Vitalik Buterin, and the founder of Luminar (makes LIDAR sensors for self-driving cars), Austin Russell, to name a few. Peter Thiel’s program has groomed many of the young, talented students of our times and given them the opportunity to do something that they’ve wanted to do, without the worry of capital.

Other than that, he’s also listed under Forbes 30 under 30, and Silicon Valley Business Journal’s 40 under 40. Girouard shared that while Gu is a brilliant tech person, he’s very understated. He doesn’t like to use fancy words to make what he’s doing sound exciting.

In an interview, Paul Gu shared about his background:

So when I was in school, I was studying Computer Science and Economics at Yale and spent time sort of preparing myself for a sort of life in a sort of quant hedge fund world (D.E. Shaws Group) and spent some time there, and essentially what I realized was, there were a huge number of very smart people applying novel technologies to solve an incredibly narrow problem, the problem of slightly inefficient securities prices on a variety of traded securities- and that was great. But it wasn't obvious that that was solving important problems for a lot of sort of real normal people, and I thought if you could simply take the same techniques that were used there and apply them to a problem that would affect real people, you could bring about real impact.

Gu also realized that anyone who isn't born with money has a hard time getting access to money before they built up a long, rich credit history and of course that means for the vast majority of people. This is just like how some jobs require you to have 3 years of experience for an entry-level job. There are at least some limits to their ability to get credit when they need it most and if he simply applied the techniques of machine learning in AI that had really been demonstrated to be incredibly powerful in other domains and applied them in credit lending, it could be big. That’s how the idea of Upstart’s AI credit lending model started.

3) Anna Counselman

Counselman’s entrance into Upstart was an abrupt one. She used to work under Girouard in Google and right before he left, she went to the conference room to bid farewell to him. Girouard then shared his idea to Counselman, and just two weeks later, the 3 co-founders were sitting together in a conference room at Google Ventures.

Before she left Google, she was the Head of Premium Services and Customer Programs. She graduated Summa Cum Laude (highest distinction) from Boston University with a BA in Finance and Entrepreneurship. She received a White House Champion of Change award and was also included as one of Silicon Valley Business Journal's 40 under 40, just like Paul Gu.

Her mission to improve credit access to the underserved is a personal one; she’s a Russian native who has personally experienced challenges in getting credit herself when she first arrived in the U.S.

Counselman is the Head of Operations at Upstart, so she’s in charge of managing the ins and outs of the company. In one of the interviews, she shared,

When you’re in that situation you could have a manager that’s just desperate to fill the position who might lower the bar a little bit to just get the person in the door. So for us, it has to be a consensus decision, and if it’s not a strong yes it’s a no. So we’ve been very very slow and deliberate at hiring. We will interview like a hundred for one for every hire that we make because that’s so critical to us as a business. But that Google model has worked for us really well.

Counselman understands that it’s her role as Head of Operations to ensure that they get the best people through their doors, and are using Google’s recruiting practices to do it. I love this. A company is only as good as the employees in it.

As we can see, this team’s management profile is stacked. Let’s take a look at what their employees are saying about the company.

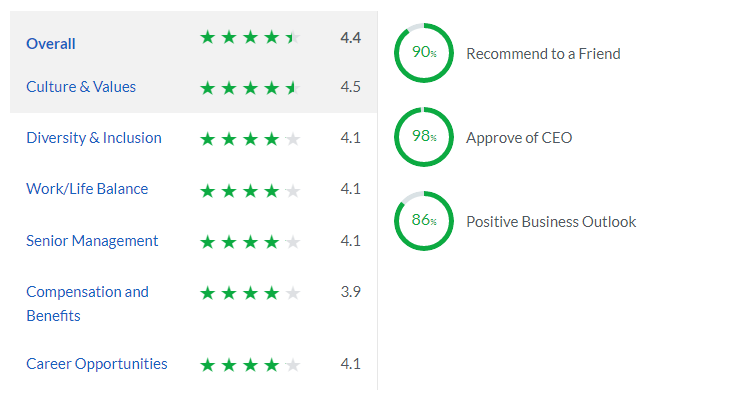

There aren't many ratings (90+) on Glassdoor for this company, given that its total size is very small, with only about 500 odd employees. Given the small population, the ratings seem pretty impressive. Their glassdoor ratings are overall of 4.4, scoring well across most of the metrics, and 98% of the reviews approve of Dave Girouard as the CEO.

When you take care of your employees, they’ll more than likely take care of your business for you. It leads to increased productivity, which leads to increased customer satisfaction, which leads to better customer retention. This results in a positive feedback loop.

Think about Costco. When they first decided to increase their salary to average $17/hr in 2004 , which was way above the industry’s standards, they were met with numerous backlash from analysts, saying that it’s better to be an employee than to be a shareholder at Costco. However, Jim Sinegal understood the flywheel effect that happens when you treat your employees well. Since then, Costco’s share price has appreciated 1000+%, compared to Walmart’s less impressive 150%. Guess it’s not too bad to be a shareholder at Costco.

It is also noteworthy that the management has skin in the game, which aligns their interests with that of the shareholders. As per their latest available SEC filing, insiders own 25.2% of the company as a whole, with CEO Dave Girouard holding 17.5% and Paul Gu holding 2.6% of the shares of the company. This includes exercisable stock options as well. I feel comfortable leaving my capital in the management’s hands.

I hope this has given you an understanding of the management. Let’s look at how Upstart makes money.

3) Business model

Upstart’s business has primarily two segments, the B2C (Business to Consumer) segment, and the B2B (Business to Business) segment. Both segments are powered using the AI model developed by Paul Gu and his team of data scientists.

1.B2C component

A customer will go onto Upstart.com to initiate their loan process, where they can apply for personal loans from $1,000 up to $50,000 with Annual Percentage Rates (APRs) between 6.5% and 35.99%. After answering a few questions, you’ll be offered a few rates within minutes given by Upstart’s partner banks.

The key difference between APRs and Interest rates is that APRs include other miscellaneous costs associated with taking up the loan like origination fees. Hence, a comparison of APRs between different loan products would be more apt compared to just looking at interest rates.

The important point about the model is that the money doesn’t come from Upstart’s own balance sheet but from partner banks and institutional investors. This means that the risk of borrowers potentially defaulting is no longer on Upstart.

Upstart does however mention that they provide funding for about 2-3% of the loans themselves, just for them to test out new products. Once they have shown that the products are able to yield satisfactory results, they’re more able to sell these new products to interested partners. It is also stated that over the last few years, the percentage of loans funded through their balance sheet has generally decreased, while the percentage of loans purchased by institutional investors and loans retained by bank partners has generally increased.

2.B2B component

The second segment, B2B, is probably the one that excites me more. Bank partners are able to place Upstart’s tech into their bank application through the use of APIs. This is something similar to what Twilio does for communication. Remember those one-time OTP messages you get from Airbnb to confirm your booking? They’re powered by Twilio. Or maybe when you’re waiting for updates from your Deliveroo rider on when your order is arriving? They’re powered by Twilio’s programmable SMS.

By copying Twilio’s code into Airbnb and Deliveroo’s application’s/website’s code, what’s happening is that the communication function is performed by Twilio, however to customers they won’t even know that Twilio was involved, as the entire interface just looks like the company’s.

This is exactly what Upstart provides the partner banks. Most banks would already have their own digital lending platforms, and they probably wouldn’t want to change anything. By allowing Upstart’s API to be integrated seamlessly into their own platforms, it reduces the friction of partnering with Upstart. On the surface, it seems like consumers are borrowing from the partner banks, but what really is happening is that the partner bank is utilizing Upstart’s AI to define the “True risk” of the borrower, before deciding whether to issue the loan and how much they should price it.

The direct bank partner channel allows partners to configure many aspects of their lending programs, including factors such as loan duration, loan amount, minimum credit score, maximum debt-to-income ratio, and return target by risk grade, as they originate consumer loans under their own brand, according to their own business and regulatory requirements. In December 2020, Upstart also launched a bank reporting portal that provides their bank partners with a centralized console to view real-time performance metrics of their lending program, view and verify their credit policy and program configuration.

In June 2021, Upstart also announced a new partnership with NXTsoft, stating that its AI platform integration with bank partners will be facilitated by NXTsoft, whose OmniConnect solution has established API connectivity to financial institutions (99% of all US-based core systems), which will allow Upstart’s bank partners to quickly integrate Upstart’s AI platform into their existing offerings.

Having more partners is crucial to Upstart’s strategy, as it will have more data to fuel its AI model, which can in turn improve the quality of the offers it can make to the consumers. This drives more consumers to take up loans originated from Upstart. Loans originated directly from the partners have a higher margin (67% vs 44%) due to the lower acquisition costs needed to acquire the consumer.

As of August’21, the CEO mentioned in its latest earnings call that there are more than 25 bank partners now, which is definitely a good sign to see, given that when they IPOed they had only 10 bank partners (150% increase!) as per their S-1. One of my concerns initially was that Upstart has been started since 2012, even though the actual model took some time to be ready, why would it only have 10 partners after 8 years if its AI/ML model is as impressive as what they state? Given that they’ve grown their partners more than 150% after they IPOed and that the time to onboard a partner has dropped to less than 90 days in some cases, has definitely eased my worries slightly about product-market fit.

For the first time, one of our bank partners decided to eliminate any minimum FICO requirement for their borrowers. To us, this demonstrates both a commitment on behalf of this bank to a more inclusive lending program, as well as an increasing confidence in Upstart's AI-powered model.

Dave Girouard on the Q2 2021 conference call

This move by the bank partner speaks volumes of the new bank partner’s confidence in Upstart’s model, and Girouard believes that there will be future bank partners that will follow suit.

Unit Economics

When we’re looking at unit economics, we’re looking at how much Upstart can bring in for every loan that they originate. From Upstart’s S-1, it mentions that revenues are primarily earned in the form of 3 usage-based fees, which can be either dollar or percentage based depending on the contractual agreement.

1. If a customer starts on upstart.com to find a loan, Upstart charges its bank partners a referral fee of 3% to 4% of the loan's principal amount.

2. If a customer uses the partner bank’s white-label Upstart application/platform to originate the loan, Upstart charges the partner a platform fee of 2% of the loan value.

3. Upstart also charges the holder of the loan (either a bank or institutional investors) an ongoing 0.5% to 1% annualized servicing fee, based on how long it takes for the customer to pay back the loan.

Upstart also provided a comparison between the contribution margin (similar to gross profit) that a Upstart.com referred loan vs a direct bank partner channel sourced loan will bring:

As we can see, a Upstart.com referred loan actually brings in more fees, net of variable costs. The main difference between both types of loans is that the Upstart.com referred loan earns Upstart a referral fee from the Partner bank, and Upstart needs to pay a Borrower acquisition fee to loan aggregators like Credit Karma, who helps Upstart acquire a borrower from their website. However, when a consumer approaches a bank partner directly, it actually allows Upstart to generate a higher contribution margin for the company.

The CEO, however in Q1’s earnings call mentioned that Upstart is indifferent between whether a consumer approaches them from upstart.com or goes directly to their bank partners.

Let’s move on to why I think Upstart will be the winner and leader in the AI lending space for the years to come.

4) Competitive advantages

Here are some commonly known advantages that Upstart brings to its borrowers and partner banks:

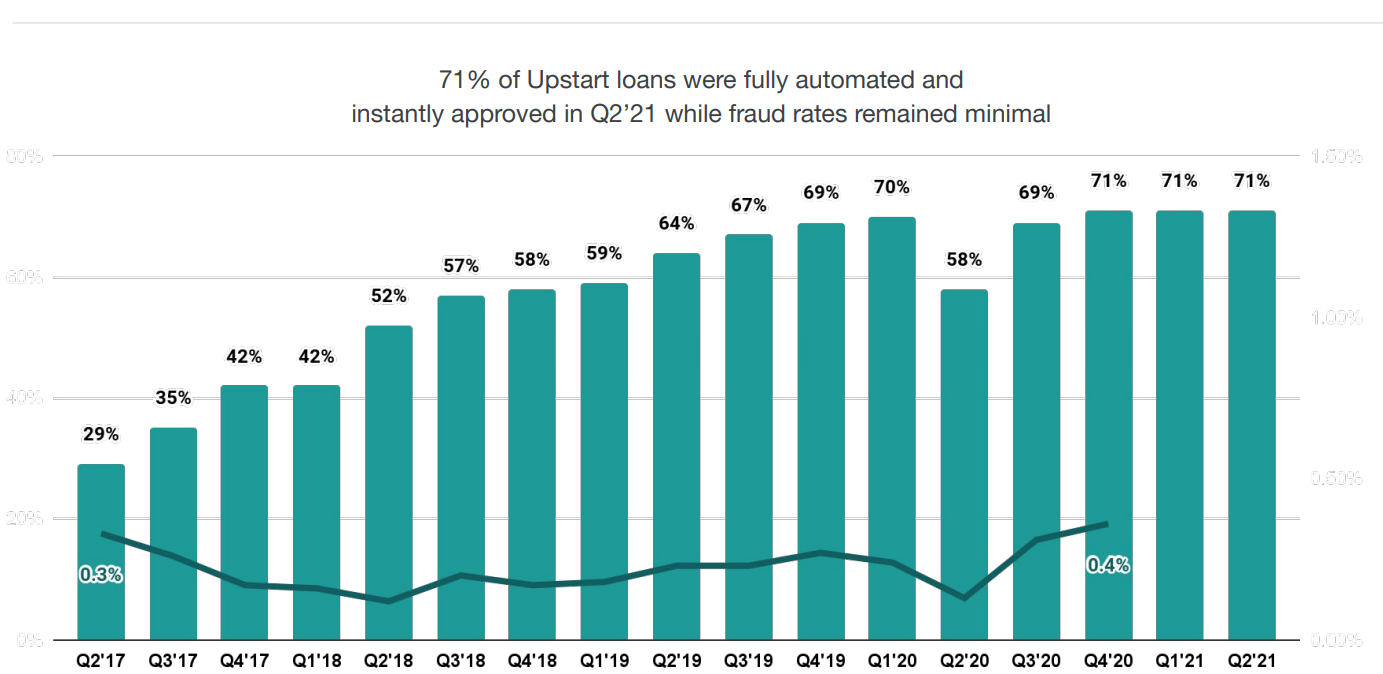

a) 71% of loans are fully automated as of 30th June 2021.

For some context, the company started out with 0% fully automated loan origination in Q3 '16 , and is currently at 71% of loans that are fully automated. I think this is a huge selling proposition to both borrowers and partner banks. When loans are fully automated, it means you no longer need credit specialists to approve a loan. This means resources are freed up, giving partner banks manpower cost savings, and these savings can be better utilized in other areas. Upstart also stated that 99% of applicants receive their money in just one business day after accepting the offer, at 10% lower average APRs for approved loans.

What are borrowers looking for when they look to take up a loan? They probably want to get the loan quickly and in a seamless process. The entire ease of getting the loan approved in real-time, without any documentation or human intervention, is something that borrowers will look for. Why would you want to wait a few days for the money to come in when you can get it the next day, with a better APR?

b) Upstart model vs. traditional bank models

Upstart also did internal studies on credit models. With the use of Upstart’s AI model, it could enable several large U.S banks to lower loss rates by almost 75% while keeping approval rates constant, while approving 173% more loans at the same loss rates. If this doesn’t show the efficacy of their AI model relative to the traditional banks, I don’t know what else does.

c) Realized Loss Rates vs. Rating Agency Model

For pools of securitized loans in eight loans between June 2017 and February 2020, Upstart’s realized loss rates were 32%-54% lower than those predicted by Kroll (rating agency), and over the same time period the realized losses for the same pool of loans were only on average 5% different than internal forecasts. When we compare this to other digital lenders, Upstart’s realized loss rates are miles ahead of other competitors.

d) Amicable relations with regulation

Financial services or Fintech are amongst the most heavily regulated industries in the world and new technologies like Upstart’s AI lending model have to be very careful, from a regulatory perspective. CEO Dave Girouard once shared in an interview that one of his first 5 employees was actually a legal counsel because he foresaw a lot of regulatory challenges coming Upstart’s way.

Upstart has demonstrated to regulators that the company’s use of alternative variables, as well as its AI/ML model, are in line with the regulations set to ensure that Upstart’s platform doesn’t introduce bias to the credit decision process, and has developed reporting procedures to ensure future versions of the model will continue to be fair. Upstart has also received no-action letters, the most recent one from the Consumer Financial Protection Bureau in Nov 2020. A no-action letter typically has a 3-year term, and the purpose of it is to reduce potential regulatory uncertainty for innovative products that may offer significant consumer benefits.

Well, Upstart is now in our second three year No-Action Letter with the CFPB, we know of no other lending platform that has received a No-Action Letter from the bureau related to fair lending. - CEO Dave Girouard

The regulatory side of things acts as a barrier to entry for other lending platforms that wish to use AI models for their business.

5) The Numbers

Upstart (UPST) reported its earnings on 10th August, and the numbers were mind-blowing. In this section, I dive into the key numbers and metrics for the most recent quarter. I wrote this as an article for Potential Multibaggers service. There’s a 2 weeks trial if you’re interested!

In my previous article on Crowdstrike (CRWD), I mentioned that revenue is one of the most important numbers I look at in the companies I own. A company’s revenue results are just like elections; just that customers are using their money to vote for the best product out there. As much as a company can cut costs, in order to grow the bottom line (profits), the top line (revenue) needs to grow first or it's unsustainable. When the revenue is growing rapidly, you can tell that there’s a product-market fit, and people are just flocking to the product.

As you can see from the table comparison above, you can definitely tell that Upstart’s execution right now is world-class. It is a given that a high-growth company needs to produce high y/y revenue growth, but when a company produces revenue growth of 60% on a quarterly (!) basis, that’s exceptional. Of course, we need to be aware that the reason why the revenue growth is at 1018% y/y is due to Q2 '2020, which was a very weak quarter as a result of a slump in loan demand because of the pandemic. However, Upstart has definitely shut down their naysayers with this quarter’s phenomenal growth, although they will probably return fast. They always do.

The contribution margin (comparable with gross margins at other companies) was also very high at 51.7%, and while the company sees it contracting in the coming quarters, it expects the elevated margins to be more durable than it had predicted at the start of the year.

The conversion rate at 24.4% was the highest it has been for the past 9 quarters, and the CFO attributed it to the success of Upstart's marketing programs, improvements in conversion funnels, and the AI model that makes the consumer product better. As a reminder, conversion rate refers to the number of loans transacted in a period divided by the number of rate inquiries received.

Another metric that I pay attention to is the automation of loans. The fully automated loan's rate has remained constant at 71% for the last three quarters, which is a good sign given that the number of loan originations has gone up 69% from the previous quarter.

As for operating expenses, the single largest expense is sales and marketing (39% of revenues), which increased y/y by 1,297%. The main reason is due to a temporary reduction in advertising expense during the pandemic, hence on a y/y comparison it seems huge. But it was 31% of revenues last year, which means it’s only up by 8% this year. For the rest of the operating expenses, there are signs of significant operating leverage. For instance, R&D expenses which used to be 44% of revenues last year, is only 16% this year! This is even with a 310% increase in R&D expenses.

The numbers were so jaw-dropping that this was what the analyst on the earnings call had to say:

Seems a bit understated when you're talking about quadruple-digit growth, which might be a first in my career. What's more impressive is as you mentioned early on, this was on the back of an -- even if you take that out, that Q2 of last year was you turned off revenue. So -- but if you compare it to Q2 of '19, you're still looking at fivefold growth on that year. And if you look at the TransUnion data and other data on the personal loan market, obviously, the personal loan market is still down as credit card balances have fallen.

Nat Schindler, BOAML Analyst

This comment by the analyst literally made me smile. Even with the headwinds of lower demand for personal loans (probably due to the government stimulus, Covid uncertainty), credit card balances are the lowest in a while, and saving rates are going up, the company is still producing these kinds of numbers. Imagine what would happen to the results when the headwinds are no longer there? And coupled with the auto loans revenue that’s going to slowly come in?

CEO Dave Girouard also said that the results have also exceeded the company’s internal expectations!

Guidance

For Q3, Upstart expects:

a) $205 to $215 million in revenue vs. $161.6 million expected by analysts

b) Contribution margin of 45% up from 42% indicated last quarter

c) GAAP Net income of $18 - $22mil

d) Adjusted EBITDA of $30 - $34mil

Management is also expecting 2021’s revenue to be $750mil, which is a whopping 25% raise from the previously indicated $600mil. I haven’t seen a company raise guidance so much in just two quarters.

In Q1, Upstart raised its guidance from $500mil to $600mil, also a 20% raise and on top of that, it's now raising that raised guidance by another 25% in Q2. That’s a 50% extra revenue expectation added in just two quarters! And the best part is that it could be raising guidance again from $750mil. Personally, I think for the remaining 2 quarters it’s possible now that revenues hit $900mil, maybe even higher.

If you think about it, the full year 2021 guidance of $750mil after deducting the 2 quarters that have already been reported, of $121mil and $194mil, leaves us with $435mil. Bear in mind that this guidance has no meaningful contribution from the auto segment baked into it yet. This means Q3 and Q4 will need to hit 217.5mil each in order to hit their guidance. Given the fact that they have beaten estimates pretty consistently, with an impressive beat of almost 23% this quarter, I’m confident that even this incredible higher guidance may be conservative, especially given management’s very positive tone during the earnings call.

Don’t forget that all these revenue beats and guidance raises compound over time as well!

6) What I like about Upstart

There are a few points that make Upstart stand out as an investment.

1. Early Adopters of AI for lending

I recently listened to an Invest Like the Best interview with Gavin Baker, the CIO of Altredes Management, and something he said really made me think of Upstart’s competitive advantage as a firm.

“The infrastructure used to train it doesn't matter, as long as it's adequate. All that matters is the quantity of data. And it's been very well established in multiple papers from both Google and Microsoft research that for every order of magnitude increase in the data you use to train an algorithm, the quality of the AI doubles. And quality means AI is fundamentally used to make predictions, and this is the variance from zero error.

So going from 96% accurate to 98% accurate is a doubling of quality. That creates all these powerful feedback loops for large tech companies, where if data quantity drives AI quality, and you have a dominant market share position, you have this feedback loop where you have the most users, they're generating the most data, that's training your algorithms and so your algorithms are improving at a faster rate than anyone else's can improve.

This part made me stop and think for a second. By this logic, wouldn’t it mean that if any of the Big 4 banks (Wells Fargo, Citigroup, JP Morgan, and Bank of America) ever decide to build an AI model like Upstart’s, it would immediately make Upstart irrelevant, given the amount of data that Big 4 banks get to collect?

Apparently not.

According to Dave Girouard in this interview, this is a question he always gets.

Chase (referring to JP Morgan here) has been doing 100 times the number of loans that your platform has done, for decades longer. They have so much data, right? Why can’t they overnight, snap their fingers, and have an AI model much better than Upstart’s? The issue here is, the data that trains an AI model has to have a certain form. This can be simplified into rows and columns. The columns are what you know about every loan applicant. The rows are the outcomes. Every repayment, every delinquency, that’s ever happened on our platform. There’s 10’s of thousands of those rows being added every month.

That training data set, which necessarily has the rows and the columns, is growing at an insane rate. You can’t just touch a server and access data that’s sat around for years, if it doesn’t have the necessary rows and columns. It doesn’t matter how much you know about somebody if it’s not predictive of an outcome or if it’s not useful in training a model.

He then used Tesla vs Ford as an analogy. Tesla is able to collect training data to train the self-driving AI models from all their cars driving on the road. Ford, the legacy model that wants to get into the self-driving space, may have ten thousand times more cars that have been on the roads for decades longer. However, Ford will not be able to use any of that past data to inform the development of any AI models. This is why Tesla investors are saying that Tesla is far more advanced in self-driving technology than you’d imagine.

This was further mentioned in a Motley Fool interview (paywall):

There's just no shortcutting it. You can't go buy the data, you can't just go find it. It has to have been done through a process of origination and which is why we've been doing this for a lot of years. We think when others get onto it, I think they will and they should, but there's just no shortcut to that time of originating, seeing the repayments or the delinquencies happen in that model, just getting more sophisticated over time. Doesn't matter what data you have, I don't care if it's from 2020, 1965. It's historic data that doesn't really inform what you can do today.

The competitive advantage for Upstart is its proprietary algorithms, developed by an unparalleled Machine Learning team led by Gu, that now ingest an exponentially growing data set, so large that the amount of compute on AWS limits Upstart in their ability to further develop their AI models.

The more bank partners, the greater the number of loans given out, the more repayment events and training data there are, which leads to a more accurate model that produces better results for the consumers(lower APR) and partner banks (lower loss rates, higher yield). This is the flywheel effect for Upstart’s AI model. Upstart’s Machine Learning team is constantly pushing for higher model accuracy. They’re constantly adding new parameters to the current model, and whenever they push a new model into production, they’re “sure as hell” that it will be better at eliminating losses that would otherwise be in the system.

By being early in using AI to determine credit risk, I believe Upstart has a head start on the rest of the banks that will eventually be using AI one way or another as the primary source of decision making to underwrite most of their consumer loans. In a study conducted in June’21 with FIs with sizes ranging from $1B to >$100B, nearly 90% of them intend to invest in AI over the next 12 months to improve credit management. The three most commonly cited reasons are speed, accuracy, and meeting existing customers’ needs.

Just take a second to think about it, it’s unimaginable how much leverage, efficiency, and value creation can happen if you just have a model with great algorithms and clean data. It makes so much sense if you’re able to underwrite loans using AI because the economics and time savings are going to be so much better.

2. They’re smaller and nimbler

When I first started researching Upstart, I was reminded of a statement (start of the article) made by Hemant Taneja (lead investor in Livongo) in his book Unscaled. In his book, he opines that smaller companies will be able to use AI to win against giants in their industries. This is exactly what Upstart is doing, or aiming to do, by working with smaller partner banks with fewer resources to take market share away from the Big 4 banks in the U.S.

I personally work in the financial sector and understand how difficult and tedious it is for bigger banks to actually hop on new technology. They’re known for their notoriously conservative management, and they have endless levels of approval and hierarchy that they have to get through in order to even try out something. Imagine that when Upstart is rolling out their new products, the big banks would still be discussing in their risk committees the potential drawback of going ahead with a new loan product. It is because Upstart has only 500 odd employees, and when any of them has any ideas, they can just bounce their ideas off Dave Girouard and his team. They’re skipping the layers of authorities that an otherwise big bank has to go through. The speed at which a product goes to market is just much faster.

Upstart’s smaller size also gives them an advantage. Being small allows Upstart to take risks inherent in developing any type of successful AI model that only a VC-funded startup could take. For a larger bank, it is more difficult for them to follow decades of fair lending laws, and be successful at increasing the number of loans given and decreasing the loss rates.

A lot of investors claim that the Big Banks won’t be able to build an AI lending model like Upstart, given many of these AI/ML talents are working in the tech giants, and nobody wants to work in big banks. I believe that theory is largely correct, but I also believe that if the banks were to throw a lot of money into hiring the talents, they would probably be able to do so.

However, they would then be putting money into a model that’s yet to be proven, potentially putting a lot of money at risk, especially given their size. And no matter how fast they wish to catch up to Upstart, it is a matter of fact that it takes time for these loans to season. You need to give the loans time to mature and for delinquencies to come in so that these data can be used to train the model that you’ve built. For instance, having the data of 1000 customers over a period of 5 years would be way better than having 5000 customers over a period of 5 months. Upstart themselves took nine years to constantly improve and retrain their model to their current efficacy, I just don’t see how they can lose their headstart instantly.

The bigger a company is, the more regulated it’ll be. Having received 2 consecutive No-Action Letters from CFPB puts Upstart in a good position to continue its lead.

Along the way, I’m certain there’s going to be a lot of lending platforms and banks coming out with their own AI models to stay relevant. However, there can be so many copycats out there, but there can only be one master, which is Upstart. Why do you think Google is the primary search engine that most people use, instead of Microsoft’s Bing or Yahoo? My thoughts are that they not only have a better AI model with better algorithms, they also have much more data to ingest and fine-tune their current models.

3. Large Addressable Market with a long runway

a) Prodigy Software Acquisition

In March 2021, Upstart announced the acquisition of Prodigy Software, a cloud-based software provider. Prior to this, Upstart’s mainly provided only unsecured personal loans. Prodigy is an end-to-end auto sales software platform that works directly with dealers to provide digital retailing functionality for customers and employees.

Dave Girouard calls Prodigy the “Shopify for car dealerships”, helping to create the modern multi-channel car buying experience that dealerships need and consumers rightfully expect in 2021. Girouard mentions that the slick purchase experience you get from buying a Tesla is actually very limited in the auto market and that it has a long way to go.

By applying the AI lending models to car dealerships, it makes the entire purchase process as simple as the personal loan process, where the entire purchase can be done in a few minutes. Upstart also claims that they’re able to shave off $100,$200 per month off the auto loan, which is a huge deal over a long period of time.

This acquisition was Upstart’s entry into the auto lending space and also a first mover into the automated process of originating and underwriting auto loans. Auto lending is a $635B market, which is 7.5x bigger than the current unsecured personal loans market (according to TransUnion data) that Upstart is focused on. This move is not only great in diversifying Upstart’s business away from unsecured personal loans, but it is also a great customer acquisition tool for Upstart’s new auto loan product.

It’s the next target market for Upstart and therefore it's important to see whether there’s any tangible progress made in expanding its auto offerings. These were the updates provided by the management in Q2’s earnings call.

a) In January, Upstart offered auto loan refinancing in 1 state. It’s now in 47 states, up from 33 states last quarter. It can now reach 95% of the USA population. Look at the insane speed at which the company is executing here!

b) Prodigy has increased its dealership footprint by 24% sequentially, and doubled it since the beginning of the year. Impressive speed here too.

c) Upstart auto saw a 100% improvement to its conversion rate since the beginning of the year. That's great to hear.

d) Upstart now has 5 bank and credit union partners signed up for auto lending. As you can see, this is still very early but the progress made is promising.

e) More than $1 billion in vehicles were sold through Prodigy, up from $800mil in Q1.

f) The company expects the first Upstart-powered loan to be offered through the platform before the end of the year. It’s predominantly doing car refinancing at this point in time.

g) When asked about the margins profile for auto loan products, Girouard answered that he expects the contribution profit will be similar to the personal loans even though the loans will bring a higher dollar revenue per loan.

With that said, I’m extremely excited to see the plans that the company has for Prodigy Software for the upcoming years. Companies that do great often have very obvious expansion possibilities and this is one for Upstart. It will take a few years before auto loans contribute meaningfully to the total revenue but it has huge potential.

b) Credit Unions

Girouard mentioned in the Motley Fool interview,

Credit unions are really joining our platform much faster than we would have anticipated. First of all, the credit unions have an affinity for personal loans, which is a very central product and auto loans, which is our emerging new product. We definitely have a version of our product that's really simple, fast, easy, for credit unions to get up and running and we can be referring customers to them in their own jurisdiction, whatever that is, pretty quickly.

On 15 June 2021, the National Association of Federally-Insured Credit Unions, NAFCU Services named Upstart as their preferred AI lending partner. This is a bigger deal than most would think. This partnership was approved following a rigorous, independent review and voting process by the credit union CEOs. Credit Unions, by its nature, is non-profit, and is created to support the local communities they’re located in and to provide access to credit. As such, they could offer the lowest costs of capital and at the same time use Upstart’s AI platform to ensure pricing is done accurately.

This opens up another field of possible consumers to Upstart, and they’re no longer reliant on just bank partners.

c) Other flavors of credit

We want to be the biggest player in AI lending in the world. And that player is necessarily gonna be an extremely large company in 10 or 20 years operating globally and in many flavors of credit - Dave Girouard, CEO Upstart in an interview

In earnings calls and interviews, Dave Girouard has shared Upstart’s ambitions to tap into other flavors of credit. He mentioned that Upstart is well-positioned to address the $4.2T mortgage and credit card originations markets. He’s not just saying it, Upstart’s already on the lookout for their Product Manager for Mortgage. Upstart originally posted this on their website but subsequently removed it. (h/t to @eugeneng_vcap and @dhaval_kotecha)

In the Motley Fool interview, he also shared that there’s a possibility of Upstart going into payday loans and also business receivables financing one day.

The sky’s the limit here, I think!

Girouard claims that Upstart could still grow into the unsecured personal loans and auto loans categories for the next 5 years, without even coming close to running up against a TAM ceiling!

4. They’re mission-driven

I love this video by Simon Sinek, a book author, and inspirational speaker. In this TED talk, he explains why some companies like Apple are able to achieve things that seem to defy all of their assumptions. He shares his theory of the “Golden Circle”.

Simon Sinek asserts that the most successful organizations know WHY they do what they do. It is the very reason the organization exists. People don’t buy what you do; they buy why you do it.

When I looked at Livongo Health when it was $40/share, I remember having an epiphany when I looked at their Glassdoor and saw what their employees were saying. “We are making a huge difference for people with chronic conditions.” Back then, I thought to myself this was the company Simon Sinek was referring to; a company where the employees know the value that their company can bring. When employees feel motivated and purpose-driven, they’re more likely to show revenue growth and this is backed by statistics.

Going back to Upstart, their mission statement is simple and clear, “Enable effortless credit based on true risk.” Upstart’s management goal is to empower everyone to achieve financial fitness, a state in which finances no longer constrain people but rather enable them to do what they want in life. The founders early on understood how important it is for borrowers to get credit. Paul Gu mentioned in his interview that he felt he could apply the AI techniques he used for his hedge fund in a real-world problem that could help many people. Anna Counselman herself, a Russian native had difficulties accessing credit when she first came to America. Dave Girouard is constantly sharing how their AI tool can bring positive changes for the average American consumer. This mission is personal for them.

According to Upstart, 4 in 5 Americans have never defaulted on a loan, but only 48% of them have access to prime credit. There are only 48% of Americans who have access to prime credit, but 80% of Americans. With Upstart’s AI model, they claim they are able to approve twice as many borrowers, with fewer defaults. This is the reason Upstart exists.

Of course, when a company is mission-driven, it shows in its products as well. Upstart’s loans have an excellent review of 4.9 on Trustpilot! Common reviews given are

Extremely easy application and approval

Done completely online without any human contact

The process was completed in less than 15 minutes!

Upstart also has a Net Promoter Score of 82+, compared to <30 in top tier banks!

Risks

Every investment comes with its own set of risks. For Upstart, its risks actually kept me away from it initially, but I think the company has been taking tangible actions against it. An investor in Upstart needs to be aware of the risks they’re taking, especially given the extremely positive sentiments following its stellar quarter.

1. Fee Concentration Risk

If you’re an investor in Upstart, you probably know Cross River Bank (CRB) accounts for a significant portion of their revenue. CRB is essentially a conduit to a vast set of more than 100 capital markets partners (institutional investors, credit funds), who actually buy Upstart loans. Being a conduit basically means CRB is responsible for channeling the loans originated to these capital market partners. Only ~25% of the loans are kept by the bank partners who originate them, while the rest are sold to the capital markets partners of CRB.

In the most recent SEC filing for Q2’21, CRB accounted for roughly 62% of Upstart’s revenue. While this has improved slightly from previous periods, this is still a huge concentration risk and is one of the few reasons my position for Upstart is not as large as I’d want it to be. There’s no sign of their relationship souring, but if for whatever reason this relationship doesn't work out in the future, it would be disastrous. Even the 2nd biggest bank partner accounted for 23% of their total revenue. This means the two partners added up already accounted for 85% of Upstart’s revenues for the first 6 months!

Remember how Fastly’s share price plunged when they lost a majority of Tiktok’s business? Tiktok was 10-11% of Fastly revenue at that point in time, and I wouldn’t want to imagine Upstart losing CRB as a partner. A question to me at this point would be, how easy is it to actually replace CRB as the conduit for Upstart originated loans?

I personally believe that this concentration risk will drop as larger partners (e.g. Associated Bank) are onboarded and start offering loans to borrowers and that as much as Upstart is reliant on CK, CK is equally reliant on Upstart.

2. Traffic/Marketing Concentration Risk

The second risk is what I call Traffic/Marketing concentration from Credit Karma (CK). CK is mainly a loan aggregator that helps consumers get free access to their credit scores and monitor their credit and then see offers of credit from lending platforms like Upstart. Upstart currently relies heavily on CK’s traffic for loan originations on their lending platform. In the latest SEC filing, it is noted that 49% of loan originations were derived from CK for the first 6 months of 2021.

The precarious point here is that under their agreement, either party may terminate their arrangement immediately, with or without cause, by providing no less than 30 days’ notice. Upstart has also opted not to participate in CK’s recent program that helps direct more customer traffic to the respective loan providers, which has reduced the number of applicants directed to Upstart by Credit Karma. I think this is their way of trying to be less reliant on CK in the future, which I think is the right move here. CK was also recently acquired by Intuit, which brings the possibility of them eventually becoming one of Upstart’s competitors, even if there are no such signs yet.

CEO Dave Girouard shared that during the COVID period, Upstart was one of the few platforms that were still up and delivering credit to consumers. So they’re actually mutually concentrated on both sides, meaning both of them are as dependent on each other. According to him, direct channels are actually the fastest-growing channels (via Facebook or consumer visits Upstart.com directly) now, slowly outpacing the growth from CK.

In the latest earnings call, CFO Sanjay Datta mentioned that Upstart spent more on marketing, from $46 mil to $71 mil in the recent quarter, and this marketing spend has shown results very quickly, as the funnel became more efficient as spendings went up.

It's just kind of underlying that is the continued strength of the funnel. And then in terms of channels, we are definitely seeing a lot of our strongest growth in channels that are more sort of direct to the consumer and to the borrower. So concentrations in marketing channel distribution are definitely declining across the board.

Even though there isn’t a mention of the percentage of originations derived from Q2’21, my guess is that it’s lower than the 49% stated for the first 6 months of 2021.

Reliance on CK is also somewhat a marketing concentration. Think about the number of businesses that rely on Google and Facebook Ads to run their businesses. Aren’t they facing the same issues as well? Businesses are constantly trying to get away from these 2 main channels, but they eventually always fall back to the same channels just because the amount of reach you get is just very different. However, it would definitely be ideal for Upstart if they can reduce their reliance on CK in the long run, and we’ve definitely heard progress from CFO Sanjay Datta.

3. Cyclical Risk

I tend to not like buying into companies that are cyclical. Being cyclical means that the revenues of the company depend largely on the economy. Upstart as a company is heavily affected by the spending in the economy, when there is more spending, there is a greater need for credit.

We all saw how the company’s revenue got hit during Q2’20 when the pandemic put everything to a halt. Nobody was sure what was going to happen, and they wouldn’t want to take on extra risk in the form of credit. This resulted in a 73% q/q drop in revenue from Q1’20. Even though many of Upstart’s bank partners noted that Upstart’s loans were significantly outperforming other lending platforms in terms of default rates from Covid to the end of 2020, borrowers will be less keen to take up more credit when there’s uncertainty in the economy. The stability in Upstart’s model has allowed their business to recover quickly within a short period of time.

Furthermore, given that the interest rates are artificially kept low for now to stimulate the economy, eventually, there will be an increase in rates from the historic low. When that comes, there may be fewer borrowers overall which would, in turn, lead to less business for banks and fewer fees collected by Upstart. This will definitely affect Upstart’s growth if it happens.

These are out of Upstart’s control.

8) Competitors and the Valuation

Lastly, let me touch a little on the competition and the valuation. Valuation for Upstart is a tricky one. The only recurring revenue that I could think of for Upstart is the servicing fees that they receive from the holders of the loan over the period that borrowers take to repay their loan. It doesn’t have the subscription model that most SaaS companies have, so it should not be valued in the same way.

As for competitors, are there any real comparables out there in the market? Here are some of the possible competitors in the lending space:

1) Big traditional banks. Lending is like the bread and butter of a bank. They basically lend out money from customers’ deposits and earn by charging higher interests to their loans compared to the interests they pay to their customers for their deposits. As mentioned above, it is definitely possible that they will venture into using AI to underwrite loans, but I don’t see this as a threat at the moment.

2) Smaller banks. The reason why smaller regional or community banks will partner with Upstart is that they do not have the AI expertise or budget to build their own AI lending platform. This is why Upstart sees itself as allies of these smaller banks, sharing with them their API, giving them a shot at competing with the bigger banks for market share in lending. Eventually, banks will need to either build out their own and partner with Upstart to stay relevant in the lending space.

3) Lending/ Lending Exposed platforms.

LendingClub(LC) is a FinTech lending platform but its shares have largely underperformed due to 2 main reasons, its ex-CEO was indicted on fraud charges, and its platform has had issues with default rates. Its share price is down 77% from IPO levels, which says a lot. However, in its most recent quarter, it grew its revenue by 93% QoQ and even raised its FY guidance. It has provided the same FY guidance as Upstart but is valued at 5.4x lesser than Upstart. The market is telling us who it believes will be the eventual winner.

LendingTree (TREE), on the other hand, is an online lending marketplace, which is a completely different business as compared to Upstart. It does not use AI/ML, and it allows potential borrowers to connect with multiple loan operators to find optimal terms for loans, credit cards, deposit accounts, insurance, etc.

4) FinTech Platforms:

FinTech platforms like SoFi(SOFI), Square(SQ), and Paypal(PYPL) lend directly to their consumers. FinTech companies have a huge advantage compared to the traditional banks given that they have a much low customer acquisition cost and they do not have to cover brick and mortar expenses. CEO Dave Girouard has mentioned in earnings calls that it’s not worried as these companies do not offer unsecured lending to consumers, which is Upstart’s main product for now. And given that Upstart has been in the AI lending space for this long, it has the headstart in using AI to underwrite a loan. Borrowers will eventually flock to whichever platform offers better rates with a better online experience, and bank partners will go to the platforms with the best underwriting capabilities.

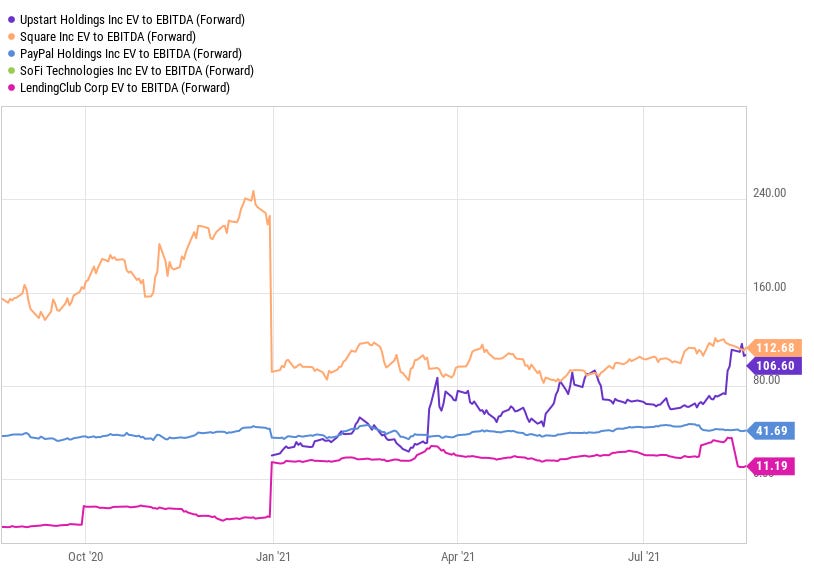

Looking at its share price, Upstart has rewarded its shareholders handsomely ever since it IPOed, but this is not a surprise given the performance it has had over the same period. Name me another company that revises their FY guidance 2 times in a year and still manages to beat their estimates by a long shot, I’ll wait.

Just by looking at these 2 charts above, Upstart screams “overvalued!” I agree that it’s expensive, but I believe quality companies will always surprise their investors with the upside. Growth rate matters and a company that is going to be growing revenue at high rates (>50%) should have very high EV/S and EV/EBITDA ratios!

To put it into perspective, a company growing its revenues at 60% for 2 years will have more than 2.5x its current revenue! And if they grow another 60% in the 3rd year, that’ll be 4x its current revenue! That’s the magic of compounding and it’s going to reduce both ratios very rapidly. Just a reminder: Upstart reported 241mil in revenues in the whole of 2020 and 195mil in their latest quarter!

There isn’t a single best metric to value a company like Upstart, and DCF just doesn’t work for a company like Upstart. What estimates do you give for a company that raises its guidance from $500mil to $750mil in the same year? That’s a 50% increase!

The flaw in DCF models is that it assumes declining rates of growth for companies, even when there are businesses that are able to sustain their growth at a high rate for a long period of time. Some businesses even accelerate their growth from prior years due to new products/avenues of growth. These are the kinds of investments that I’m looking to make. It’s rare, and because it’s rare these companies are usually priced very highly.

The auto loans segment is going to start bringing in revenues in FY22, and the new partners and the line of partners that Upstart has onboarded/is going to onboard are going to bump up revenues in the coming quarters. We have not even factored into the growth once Upstart eventually enters the Mortgage segment.

Upstart originated $2.8B in Q2’21, if we annualized it, assume 0% growth, it’ll be $11.2B, which means Upstart has a 13.2% market share right now. I believe Upstart will continue to chip away market share from the incumbents, given its superior underwriting capabilities.

If the company is able to garner a market share of just 2.5% for its auto loans in FY22, it will be $12.7B originations! We can assume the company will get a larger pie as time goes on. A 10% market share in auto loans is $63.5B (based on latest estimates), which is already 5x of Upstart’s current originations! It will definitely take time for Upstart to get there, but you see what I’m getting at.

Now, are you still wondering why the company is priced so high?

Final Thoughts

I can assure you that there will be lots of noise along the way, but you can ignore the noise if you’re going to be a long-term investor. You just have to know that Upstart is moving their AI model into more verticals at a neck-break speed, and these new segments are not even factored into their guidance yet. The recent numbers are proof of the company’s phenomenal execution and you don’t need to be a genius to know that the company’s on the right trajectory. I’m not sure how the stock will perform in the next few weeks/months, but I believe that Upstart has a shot at its ambitions of becoming one of the biggest Fintech companies in the world.

Upstart’s results this quarter have given the best earnings report thus far of all the companies I own. I didn’t own a large position initially because of the abovementioned risks, and I wanted to confirm that the management is able to deliver after raising their guidance, and they have shown that they can. I will definitely add on to my position in the event of corrections, and I believe Upstart’s performance from here will surprise many, to the upside.

Disclosure: I’m long $UPST, and this article is for informational purposes and should not be taken as buy/sell advice.

Since your article a LOT has changed both at macro level as well as micro (QoQ revenue dropped from 60% in Q2 to about 16% in Q3 and anticipated to drop to 12%-16% in yet to be reported Q4 on 2/15/22.

What are your thoughts on UPST as of today January 22, 2022 and after having gone through the stock reaching $400 and cut by 80% (with no light at the end of tunnel yet)?

An analyst from Wedbush today claimed there are increasing delinquencies (but of course without offering one single iota of proof and/or source of his claim). Your thoughts on this claim...?

Thank you